Impacts on Financial Institutions

These trends and adoption of resulting propositions is going to accelerate over the next five years as Open Savings and Investments standards emerge, trust of new services matures and the previous barriers to entry of manual operations and financial data aggregation disappear through digitisation.

This will enable a greater ability for consumers to selectively use and aggregate services and financial products from many providers and will make the new financial services environment necessarily collaborative, transparent and, for consumers, democratise previously unavailable expertise and services (not just products) economically viable to scale downward, making them accessible to all.

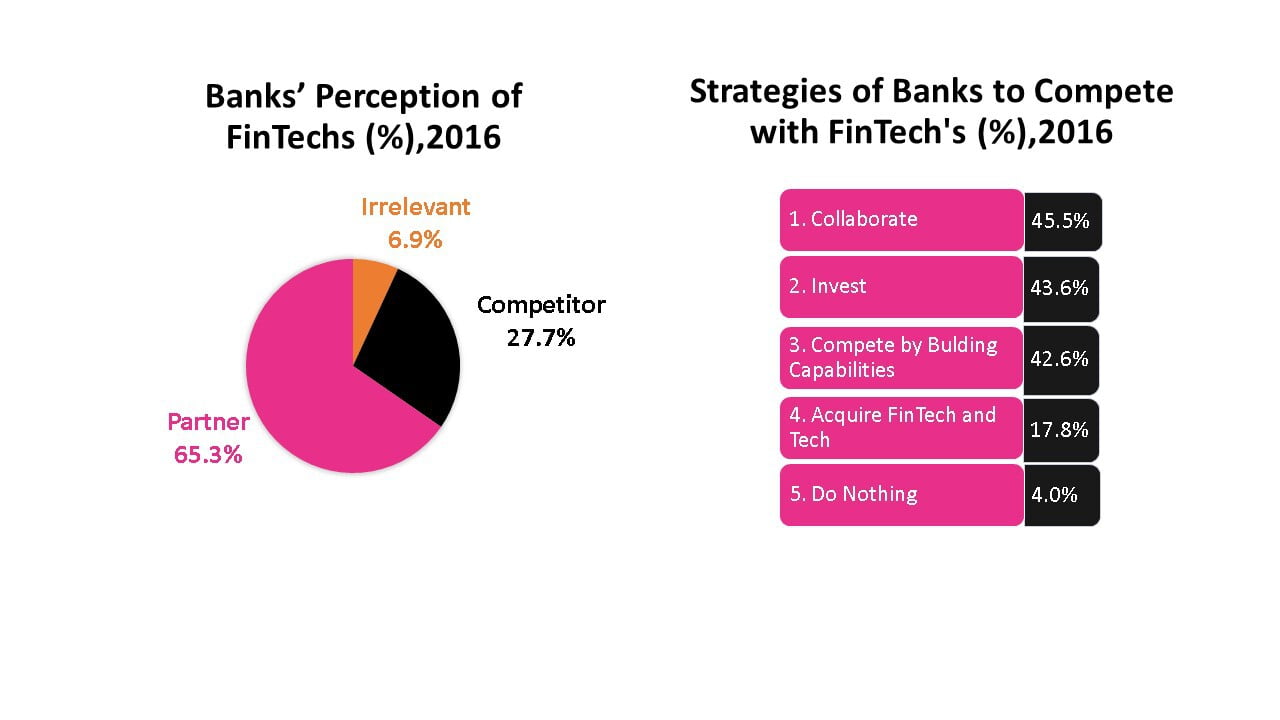

Response Strategies of Financial Institutions

Since 2016 the response strategies that most financial institutions have followed have been a combination of attempting to collaborate with FinTechs and adopt FinTech techniques.

Such agile, DevOps, micro services and the development of open APIs that could enable third parties to develop applications, services, and tools using the models and or the information stored in their databases for the benefit of others. Retail banks were the first to realise the strategic imperative and in the World retail bank survey 2016 published by Capgemini, the top strategy to deal with FinTech is to collaborate.